Now that we’ve cleared the halfway point for 2024 with retailers preparing for back-to-school shopping (and Q2 2024 reporting season), we thought we’d take stock of where we stand from a retail category perspective. Last year, we looked at visit per location data by retail category at the halfway point for the year, which proved to be a useful indicator for what to expect for the rest of the year. We thought we’d revisit the analysis to give some perspective of what to expect in the months to come.

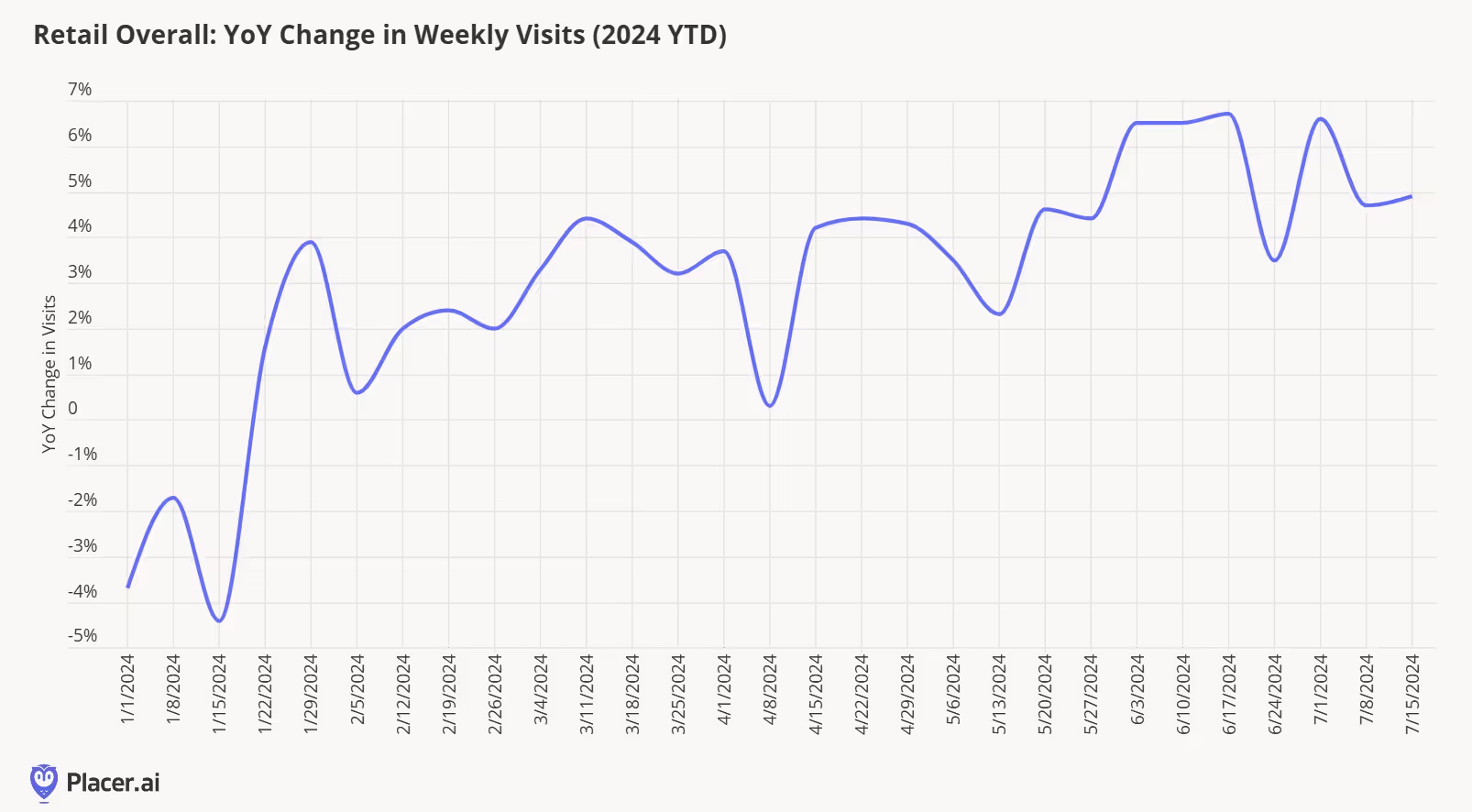

Needless to say, it’s been another volatile year for most retailers, with a tepid start to the year due to weather, followed by solid event/holiday spending in February/March, and a lackluster April (though partly the result of the Easter holiday calendar shift). May, June, and July visitation data offered some encouraging signs, with year-over-year visits increasing to a mid-single-digit level (according to Placer's Industry Trends report). Importantly, increased visits won’t necessarily translate into the same level of sales increases, as visits are continuously being driven by deals/lower price points for many categories.

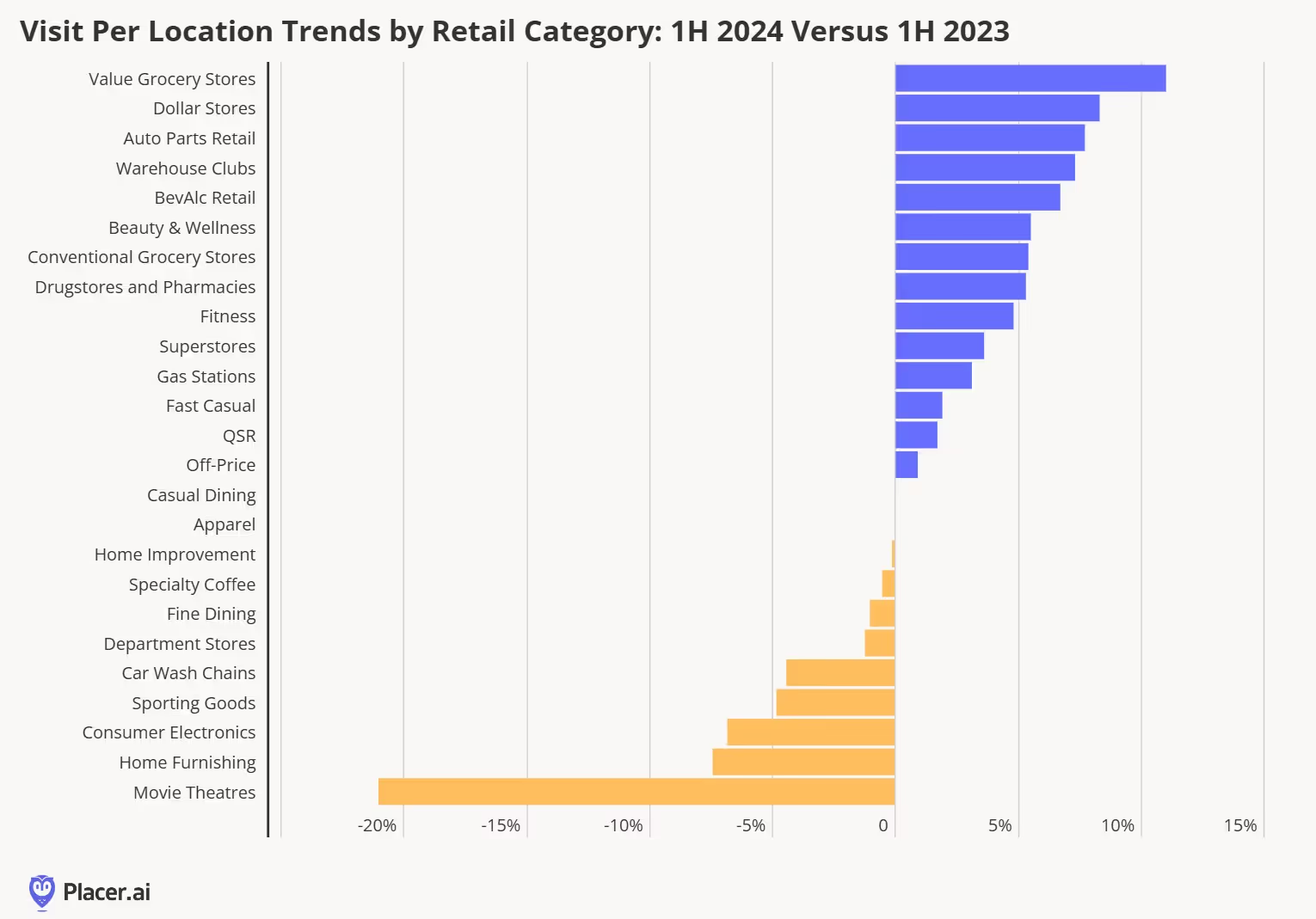

Based on the positive trendline for retail in general, it shouldn’t be a surprise that the majority of the 25 retail categories we’ve presented show positive growth from a visit per location year-over-year perspective (below).

A few notable takeaways from the visit per location analysis:

- Value grocery chains saw the largest increase in visit per location during the first half of the year, up 11% year-over-year. We’ve spoken at length about consumers’ focus on value this year–even as food-at-home prices have moderated–so it should not be a surprise to see this category seeing the most visits per location. Both Aldi and Trader Joe’s have been key contributors to the increase in visits per location.

- Auto parts retail was one of the leading categories with respect to visits per location during the first half of 2024, but these trends may be moderating as we discuss below.

- Like many of the categories seeing visit per location growth, consumers continue to seek out warehouse clubs for value. We also believe that visits from younger trade areas have contributed to the increase in warehouse club visits per location, which we recently analyzed.

- Fitness was the top category for visit per location when we looked at pre- versus post-pandemic visit per location trend last year, but trends have moderated as consumers have pulled back on discretionary spending.

- There were mixed results across the restaurant category, with fast casual and QSR seeing year-over-year gains in visits per location, casual dining running about even to a year ago, and specialty coffee and fine dining seeing year-over-year declines. The QSR and fast casual gains largely reflect consumer’s focus on value, although the visit per location gains started to slow from March-May amid more competitive pricing from grocery stores, c-stores, and casual dining. However, with the rise of $5 bundled meals across the QSR category, we’ve seen visit per location trends rebound a bit in June (and into July). Specialty coffee is down year-over-year but is largely the result of fewer visits from “occasional” Starbucks visitors (which have overshadowed the nice gains we’ve seen from many drive-thru coffee chains this year). Fine dining is down year-over-year, but we continue to see visit per location gains for major holidays and events.

- The decline in movie theaters is not surprising given the lack of tentpole releases this year. However, these trends should improve amid a stronger release schedule.

Last year, our midpoint visit per location trends gave us some ideas as to how the second half of the year might shake out. Based on our first half 2024 visitation data, we expect (1) consumers to continue prioritize value in the second half of the year, especially those chains that have been able to create excitement/newness for their value assortment; (2) consumers will continue to prioritize holidays/events, which bodes well for back-to-school, Halloween, Thanksgiving, and Christmas; (3) we will continue to see better balance between experiences and goods this year (as we've discussed in the past).

.svg)