The holiday shopping season is nearly upon us – and one category that always benefits from holiday sales is apparel. So with Q4 underway, we checked in western wear leader Boot Barn and discount footwear chain DSW (Design Shoe Warehouse, owned by Designer Brands, Inc.) to see how they fared in Q3 2024 – and what awaits them as Black Friday approaches.

A Step Up in Visits

Boot Barn and DSW – two very different shoe retailers – have been thriving in recent months. Since May 2024, the two chains have seen sustained monthly year-over-year (YoY) visit growth, finishing out Q3 2024 with visit upticks of 10.8% (Boot Barn) and 10.5% (DSW).

For Boot Barn in particular, Q3’s robust visit growth was at least partially driven by the chain’s aggressive expansion strategy: Between July 2023 and June 2024, Boot Barn opened some 50 new stores – and plans to open dozens more over the coming year. But foot traffic data also shows that the chain has succeeded in growing its footprint without significantly diluting traffic at existing locations. During Q3, the average number of visits to each Boot Barn location dipped just slightly below 2023 levels (2.8%), even as YoY visits to the chain surged by 10.8%.

DSW, for its part saw significant YoY visit growth throughout Q3, despite a store count that has remained relatively stable. As a store that offers shoppers access to high-quality, name-brand products at affordable prices, DSW lets consumers trade down while splurging at the same time.

Size Isn’t Everything

DSW isn’t called a warehouse for nothing. The typical DSW store spans about 25,000 square feet (though the chain has begun experimenting with smaller formats) – compared to just 12,000 - 14,000 for Boot Barn. But despite the smaller size of Boot Barn’s locations, visitors to the western wear chain tend to spend more time in-store than visitors to DSW. Since 2022, average visitor dwell times at Boot Barn have ranged between 34.9 and 35.8 minutes, while dwell times at DSW have hovered between 32.1 and 32.8 minutes.

Customers at DSW may be more likely to know in advance what they’re looking for, making a bee-line for the discounted footwear they’ve been waiting to get their hands on. Visitors to Boot Barn, on the other hand, may spend more time browsing the brand’s wider selection of merchandise.

The difference in visitor dwell times may also be partially due to Boot Barn’s firmer positioning as a weekend destination: Over the past twelve months (October 2023 - September 2024), 59.5% of visits to Boot Barn took place between Fridays and Sundays, compared to 56.3% for DSW.

Still, visitors to both chains tend to remain in-store for more than half an hour – revealing a highly engaged customer base eager to explore the brands’ varied offerings.

Different Seasonal Rhythms

With a strong Q3 2024 under their belts, what can DSW and Boot Barn expect this holiday season?

Looking at weekly fluctuations in visits to Boot Barn and DSW in 2022 and 2023 – compared to yearly weekly averages – reveals another striking difference between the two chains: Visits to Boot Barn peak in November and December each year, as customers descend upon the chain to purchase western-themed gifts for loved ones. DSW, on the other hand, sees greater visit boosts in spring, perhaps buoyed by shoppers updating their wardrobes in anticipation of warmer weather.

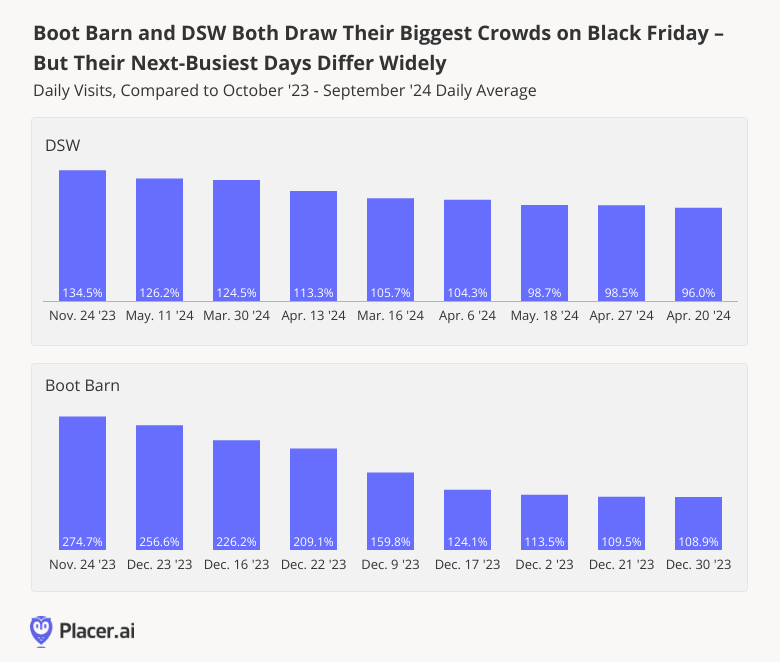

But zooming in on the two chains’ busiest days of the year tells a somewhat different story. Even though DSW experiences a more muted holiday shopping season, the shoe leader – like Boot Barn – draws its biggest crowds of the year on Black Friday. On November 24th, 2023, visits to DSW jumped 134.5% compared to the chain’s daily average for the 12-month period from October 2023 to September 2024 – a smaller spike than that seen by Boot Barn, but significant nonetheless.

After that, however, the chain’s visitation patterns diverged. For DSW, the next eight busiest days of the year were all Saturdays in Spring – including the Saturday before Mother’s Day (May 11th) and the Saturday before Easter (March 30th). For Boot Barn, on the other hand, December shopping days – including Super Saturday (December 23rd) – drove the biggest foot traffic spikes.

A Slice of Success

With holiday shopping just around the corner, DSW and Boot Barn both appear poised to enjoy a healthy Q4 – each in their own way. Which other footwear and apparel brands are likely to succeed this holiday season?

Follow Placer.ai's data-driven retail analyses to find out.

This blog includes data from Placer.ai Data Version 2.1, which introduces a new dynamic model that stabilizes daily fluctuations in the panel, improving accuracy and alignment with external ground truth sources.

.svg)